Buying your first home is one of the biggest financial milestones in life—especially in India, where property ownership is deeply tied to security and long-term wealth. However, for first-time buyers, the process can feel overwhelming due to legal formalities, financing options, and market variations.

This step-by-step guide for first-time homebuyers in India will help you make informed, confident decisions and avoid costly mistakes.

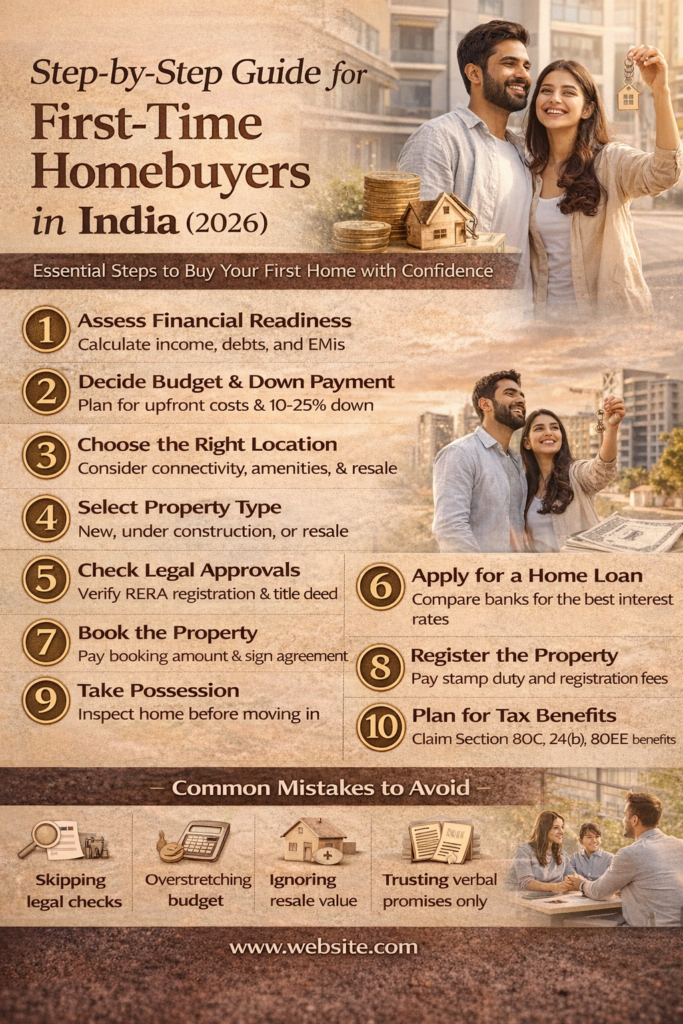

Step 1: Assess Your Financial Readiness

Before starting your property search, evaluate your finances realistically.

Key things to calculate:

- Monthly income & expenses

- Existing EMIs or liabilities

- Credit score (750+ is ideal)

- Emergency fund (6 months minimum)

💡 Rule of thumb: Your home loan EMI should not exceed 30–40% of your monthly income.

SEO keywords: first time home buyer India, home buying checklist India

Step 2: Decide Your Budget & Down Payment

In India, banks usually finance 75–90% of the property value.

Typical upfront costs include:

- Down payment (10–25%)

- Stamp duty & registration

- GST (for under-construction properties)

- Brokerage (if applicable)

- Interior & moving costs

Plan for additional 7–10% over the property price.

Step 3: Choose the Right Location

Location plays a major role in long-term appreciation and daily convenience.

What to look for:

- Proximity to workplace

- Connectivity (metro, highways)

- Social infrastructure (schools, hospitals)

- Future development plans

- Safety & livability

📍 Tier-1 cities like Mumbai, Pune, Bengaluru, Delhi-NCR, Hyderabad and emerging Tier-2 cities are popular among first-time buyers.

SEO keywords: best cities to buy home in India, property location checklist

Step 4: Select the Right Property Type

Decide what suits your lifestyle and budget:

- Ready-to-move: No GST, immediate possession

- Under-construction: Lower price, GST applicable, delivery risk

- New launch: Attractive pricing, longer wait

- Resale property: Prime location, negotiation possible

Choose between apartment, villa, or gated community based on needs.

Step 5: Check Builder Credibility & Legal Approvals

This step is critical to avoid future disputes.

Must-check documents:

- RERA registration number

- Approved building plans

- Title deed & chain of ownership

- Encumbrance certificate

- Occupancy Certificate (for ready homes)

🔍 Always verify details on the RERA website of your state.

SEO keywords: RERA approved projects India, property legal checklist India

Step 6: Apply for a Home Loan

Compare home loan options from:

- Public banks

- Private banks

- Housing Finance Companies (HFCs)

Key factors to compare:

- Interest rate (fixed vs floating)

- Processing fees

- Prepayment charges

- Loan tenure

📄 Get a loan pre-approval to strengthen your buying position.

Step 7: Book the Property & Pay Booking Amount

Once satisfied:

- Pay the booking amount

- Sign the Agreement to Sell

- Ensure all payment milestones are documented

Never make large payments without proper receipts and agreements.

Step 8: Register the Property

Property registration legally transfers ownership.

Includes:

- Stamp duty payment (varies by state)

- Registration fees

- Sale deed execution

After registration, ensure the property is mutated in your name in local records.

Step 9: Take Possession & Do a Final Inspection

Before taking possession:

- Inspect for construction quality

- Check fittings, plumbing & electricals

- Ensure amenities promised are delivered

Collect:

- Possession letter

- Keys

- Maintenance details

Step 10: Plan for Tax Benefits

First-time homebuyers in India can enjoy multiple tax benefits:

Under Income Tax Act:

- Section 80C: ₹1.5 lakh (principal repayment)

- Section 24(b): ₹2 lakh (interest on loan)

- Section 80EE / 80EEA: Additional benefits (subject to eligibility)

Consult a tax advisor for maximum savings.

Common Mistakes First-Time Buyers Should Avoid

❌ Ignoring legal verification

❌ Overstretching budget

❌ Not checking resale value

❌ Skipping home inspection

❌ Relying only on verbal promises

Final Thoughts

Buying your first home in India is a rewarding journey when done right. With proper planning, legal due diligence, and financial discipline, you can turn your dream of homeownership into a secure, long-term investment.

Taking it step by step ensures peace of mind—and protects your future.